Fed on Watch

Week of January 12th, 2026

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: xAI Leads As 2026 Is Off To A Brisk Start (Crunchbase, 5 minute read)

xAI (Generative AI): Elon Musk’s xAI raised $20 billion in a Series E, bringing total reported funding to $42.7 billion. Founded in 2023, the company develops the Grok chatbot and operates as the parent of X (formerly Twitter), with backing from a broad mix of venture and strategic investors

Parabilis Medicines (Precision Medicine): Parabilis Medicines raised $305 million in a Series F co-led by RA Capital Management, Fidelity, and Janus Henderson, to advance clinical development of its peptide-based cancer therapeutics platform

Soley Therapeutics (Biotech): Soley Therapeutics secured $200 million in a Series C led by Surveyor Capital, supporting its cell stress sensing platform and pipeline targeting neurodegenerative and metabolic diseases

LMArena (AI Evaluation): LMArena raised $150 million led by Felicis Ventures and UC Investments, valuing the company at $1.7 billion post-money, nearly 3x its seed valuation from mid-2025, to expand its AI model evaluation platform

Diagonal Therapeutics (Biotech): Diagonal Therapeutics raised $125 million in a Series B led by Sanofi Ventures and Janus Henderson, funding development of disease-modifying clustering antibodies for severe genetic diseases

Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records (Crunchbase, 4 minute read)

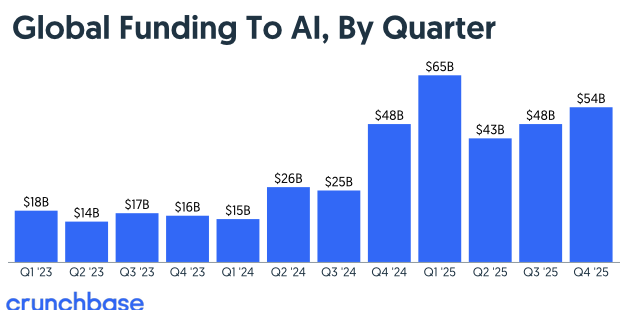

Global startup funding rebounded in 2025 after three years of stagnation, rising 30% YoY to $425 billion across 24,000+ companies, making it the third-highest venture year on record after 2021 and 2022. The year set multiple records, including the largest private funding round ever ($40B to OpenAI), the highest private valuation (SpaceX at $800B), and the largest venture-backed acquisition (Google’s $32B purchase of Wiz). The recovery was highly concentrated in AI: just five AI companies (OpenAI, Scale AI, Anthropic, Project Prometheus, xAI) raised $84B, or 20% of all venture funding

AI alone attracted $211B, up 85% from 2024, accounting for ~50% of global venture investment and surpassing all prior years

Funding momentum accelerated through the year, with Q4 reaching $113B, driven by late-stage deals

Capital remained tightly concentrated: ~60% of funding went to just 629 companies raising $100M+, and over one-third went to 68 mega-round recipients

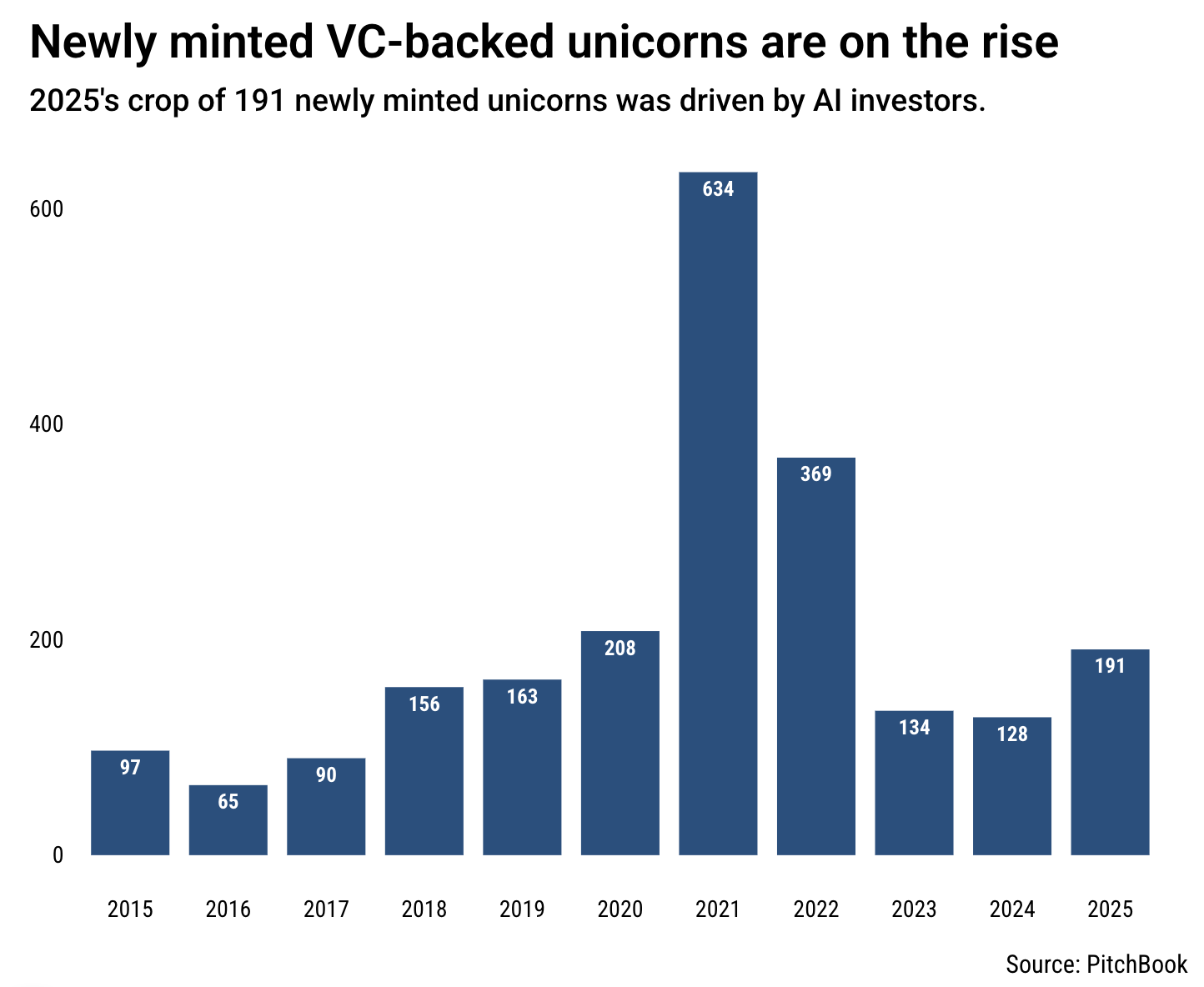

VCs minted more new unicorns in 2025 (PitchBook, 3 minute read)

AI-driven fundraising drove a sharp rise in new unicorns in 2025, with 191 startups globally reaching $1B+ valuations, up from 128 in 2024 but still below the 2021 peak. Much of the increase was fueled by large AI rounds, though investors warn of valuation inflation, particularly among companies with little or no revenue. Notable examples include Thinking Machines, which raised ~$2B at a $12B valuation before launching a product, and Kalshi, which jumped from a $2B valuation to $11B after a $1B Series E

OpenEvidence also saw rapid valuation growth, rising from $925M to $3.5B in five months and then nearly doubling again to $6B by October 2025

Some investors attribute the surge to faster growth, particularly among AI-driven startups

Others see it as a potential bubble, marked by a widening divide between a small group of rapidly scaling unicorns and the rest of the market

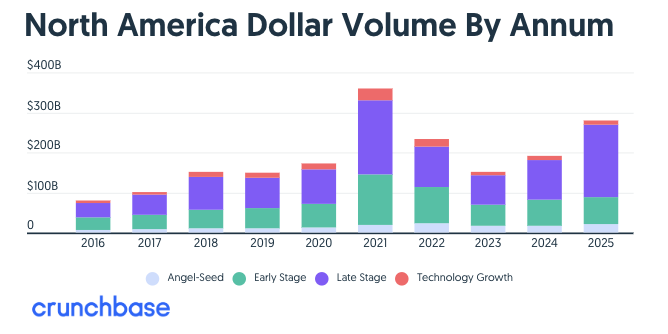

North American Startup Funding Soared 46% In 2025, Driven By AI Boom (Crunchbase, 4 minute read)

North American startup funding surged in 2025, with $280 billion invested across U.S. and Canadian companies, the highest level in four years and a 46% increase YoY, capped by a strong $67 billion Q4. While total deal count fell 16% YoY to ~10,500 rounds as capital concentrated in larger checks, funding strength was broad-based, led by AI, which captured $168 billion (≈60%), including mega-rounds such as OpenAI’s $40B and Anthropic’s $13B, and $36B in Q4 alone

Late- and growth-stage companies raised $191B for the year (+75% YoY), early-stage startups attracted ~$69B (+5% YoY, with $21.6B in Q4), and seed funding reached $20.4B, despite fewer deals

Exits also rebounded, highlighted by IPOs from CoreWeave and Figma, and major M&A such as Google’s $32B Wiz deal and Nvidia’s $20B Groq asset acquisition

ECONOMIC SNAPSHOT

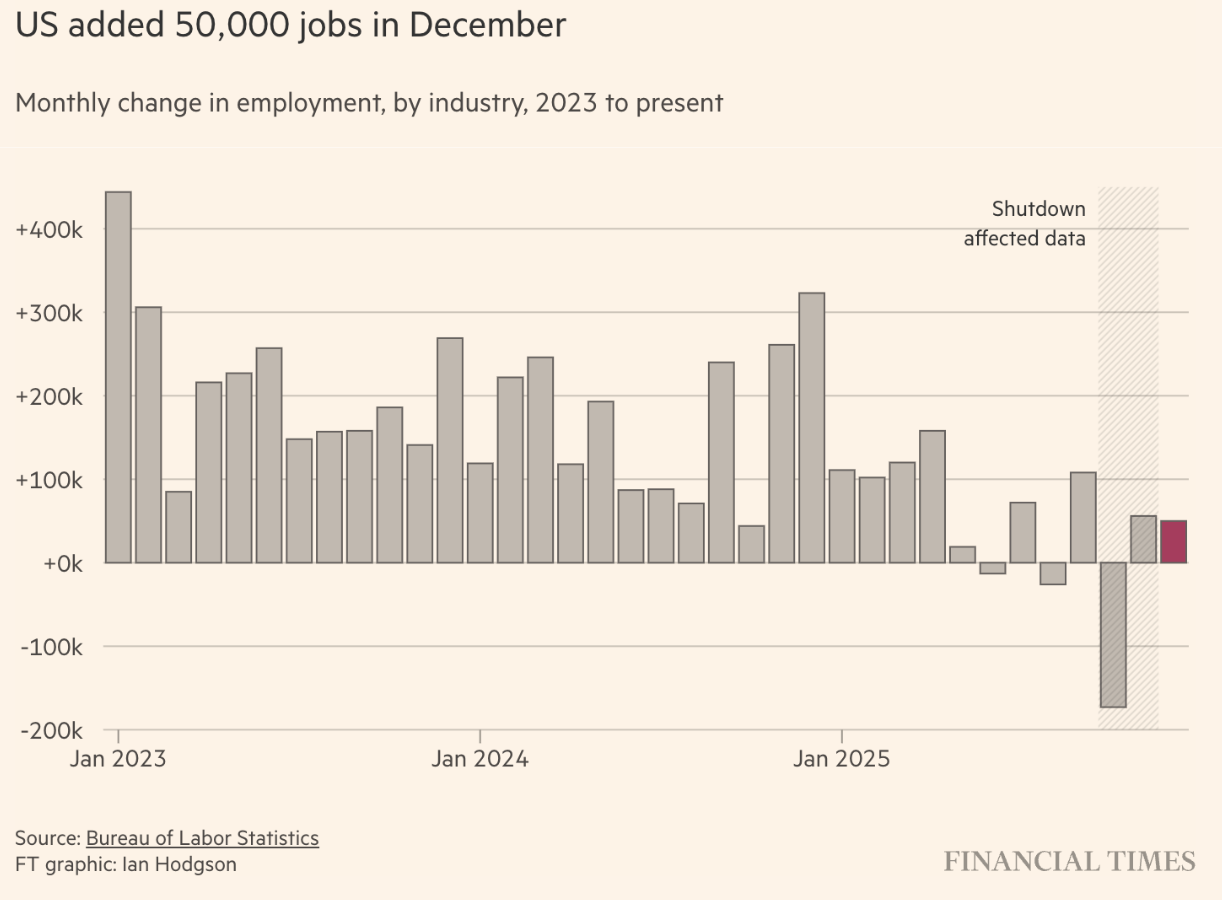

US economy undershoots expectations to add just 50,000 jobs in December (Financial Times, 2 minute read)

The US labour market showed further signs of cooling in December, with the economy adding just 50,000 jobs, below expectations of 70,000, while prior months were revised lower. Despite weaker hiring, the unemployment rate fell to 4.4% from 4.6%, surprising markets and pushing the 2-year Treasury yield up to 3.52%. The data reinforces a picture of a stagnant but not collapsing job market, following federal workforce cuts and slower private hiring

The Federal Reserve has cut rates at its last three meetings, bringing the benchmark range to 3.5%–3.75%

Economists say soft job growth combined with lower unemployment strengthens the case for the Fed to pause rate cuts in January

However, they still expect additional cuts later in 2026 as inflation pressures continue to ease

Will US inflation figures derail the Fed’s rate cut plans? (Financial Times, 5 minute read)

Investor focus is firmly on the US outlook, where markets expect the Federal Reserve to hold interest rates steady at its January meeting and deliver two 0.25 percentage point cuts by the end of the year. Those expectations hinge on upcoming inflation data, with economists forecasting headline inflation flat at 2.7% in December and core inflation edging up to 2.7% from 2.6% in November

Any upside surprise could disrupt rate-cut assumptions, especially after concerns that November’s sharp inflation drop was distorted by data issues linked to last year’s government shutdown

With US borrowing costs already at a three-year low, Fed officials remain divided

Analysts warn that if inflation fails to cool as expected, rates could move materially higher, posing a key risk for markets in the near term

Federal Prosecutors Are Said to Have Opened Inquiry Into Fed Chair Powell (The New York Times, 6 minute read)

U.S. prosecutors have opened a criminal investigation into Federal Reserve Chair Jerome Powell over the $2.5 billion renovation of the Fed’s Washington headquarters and whether he misled Congress about the project’s scope, escalating President Donald Trump’s long-running conflict with the central bank chief. Approved in November by U.S. Attorney Jeanine Pirro, the probe examines Powell’s testimony and spending records and comes as Trump has repeatedly criticized Powell for resisting aggressive interest-rate cuts and threatened to replace him

Powell has called the investigation “unprecedented,”arguing it represents political retaliation and a threat to the Fed’s independence, warning against monetary policy being shaped by political pressure

The renovation, launched in 2022 and slated for completion in 2027, is estimated to be about $700 million over budget, though the Fed says overruns stem from inflation, labor costs, and unexpected asbestos and contamination issues

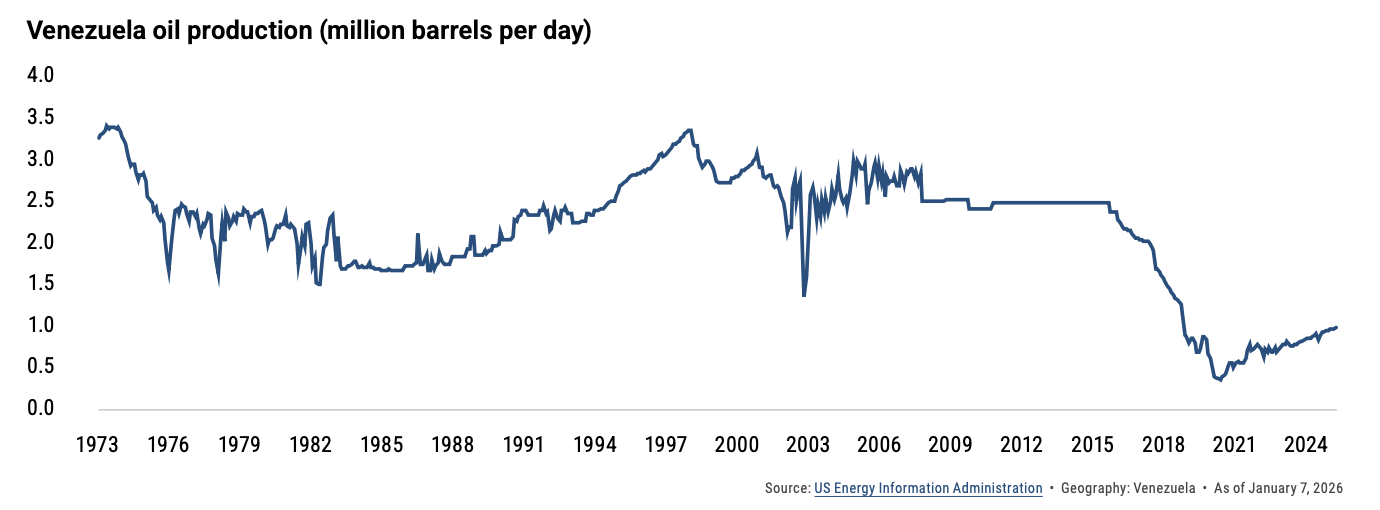

PitchBook Analyst Note: Eyes on Venezuela’s Oil Revival (PitchBook, 15 minute read)

Venezuela’s political shock has reopened access to the world’s largest oil reserves (303 billion barrels, 17% of global total), but the investment case remains challenging. Production could rise from 800–900 thousand barrels of oil per day (kb/d) to 1.5–2 million barrels of oil per day (mb/d) near term, yet returning to historical peaks of ~3.5 mb/d would require $100 billion+ and years of rebuilding degraded infrastructure. Most reserves are extra-heavy crude, with production costs of $70–$80 per barrel, above current oil prices and costlier than Canadian alternatives, limiting near-term investor appeal. For global markets, increased Venezuelan heavy crude flows to US Gulf Coast refineries could pressure Canadian heavy oil prices, deepening existing discounts

As a result, investors, particularly private equity, are expected to proceed cautiously, favoring low-risk, indirect exposure (oilfield services, logistics, midstream and power rehabilitation) rather than large upstream bets

Major US oil companies may eventually re-engage but face capital discipline pressures and competing global opportunities, making PE partnerships likely only once political stability improves and returns clearly justify the risk

IPO & EXITS

Crypto Wallet Firm BitGo, Backers Seek $201 Million in US IPO (Bloomberg, 3 minute read)

BitGo Holdings plans to raise up to $201 million in an IPO, positioning it as the first crypto company to pursue a public listing in 2026. The Palo Alto–based firm is offering 11.8 million shares at $15–$17, implying a market value of up to $1.96 billion, above its $1.75 billion valuation in 2023, with pricing expected on Jan. 21. Founded in 2013, BitGo provides digital asset custody, security, and liquidity, oversees about $104 billion in assets, and supports more than 1,550 digital assets, including serving as custodian for the USD1 stablecoin linked to World Liberty Financial

The IPO follows a wave of crypto listings in 2025 amid a more supportive US regulatory backdrop, though post-IPO performance across the sector has been mixed

BitGo reported $8.1 million in net income on $10 billion in revenue for the first nine months of 2025, up from $5.1 million on $1.9 billion a year earlier

Goldman Sachs and Citigroup are leading the IPO, with shares set to trade on the NYSE under the ticker BTGO

Goldman Sachs tops global M&A rankings with $1.48 trillion in deals (Reuters, 4 minute read)

Goldman Sachs once again topped global dealmaking league tables in 2025, benefiting from a surge in mega-mergers as 68 deals worth $10 billion or more totaled $1.5 trillion, more than double the prior year. Goldman advised on 38 of those transactions, the most of any bank, with $1.48 trillion in total deal volume, about 32% of the market, marking the strongest year for mega-deals by number since records began in 1980. The company ranked No. 1 in both M&A fee revenue and overall deal value. This came even as Goldman missed out on advising on the year’s two largest transactions, including Union Pacific’s $88.2 billion bid for Norfolk Southern

Goldman Sachs earned $4.6 billion in M&A fees, ahead of JPMorgan at $3.1 billion and Morgan Stanley at $3.0 billion

It also captured a 44.7% market share in EMEA-related M&A, its highest level since 1999

Deal activity was driven by abundant capital and looser regulatory scrutiny under a more permissive U.S. antitrust environment. Rising asset values also supported activity

Crystal Ball: How IPOs and dealmaking will shake out in 2026 (Fortune, 6 minute read)

After a strong but uneven 2025, highlighted by successful IPOs such as Circle and major M&A transactions including Google’s $32 billion acquisition of Wiz, the exit market remains selective heading into 2026. IPO activity is up from recent lows but still below historical levels, with investor demand concentrated on larger, high-quality companies, while smaller issuers continue to struggle. Many private companies are now bigger by valuation and have more liquidity options, allowing top-tier firms to delay public listings, while others increasingly pursue acquisitions or acquihires instead of standalone IPOs

IPO momentum is expected to extend into early 2026 before slowing, as a four-year backlog of tech companies works through a narrowing window

M&A is expected to stay active but uneven, with the possibility of a $50 billion-plus AI deal, more fintech consolidation, and sizable biotech acquisitions backed by over $1 trillion in cash held by large pharmaceutical companies

Secondary markets are expected to expand, with some forecasts putting private-market secondary volumes at $250 billion in 2026, as tender offers and other liquidity options become more common in a higher-rate environment

WHAT A TIME TO BE ALIVE

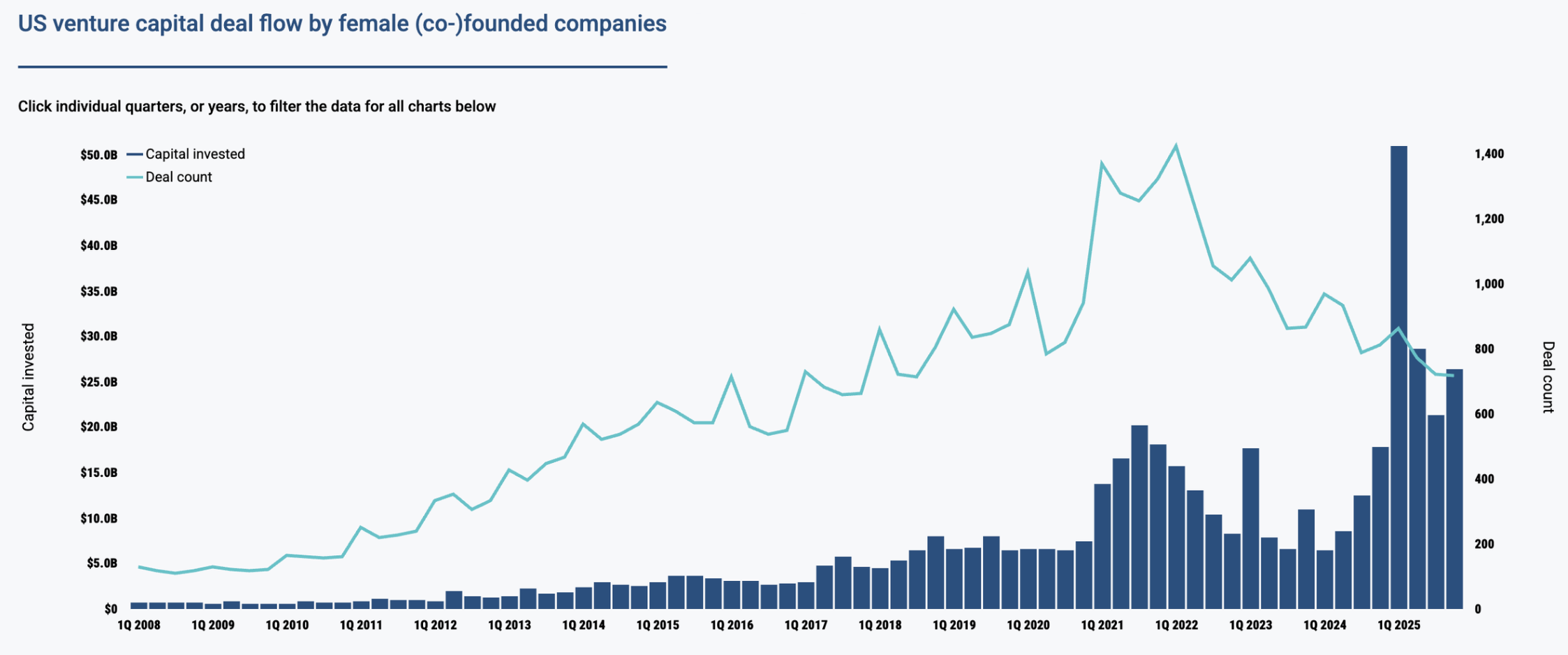

US VC female founders dashboard (PitchBook, 5 minute read)

Venture capital funding for female-founded startups in the U.S. has stabilized after a steep decline from the 2021 peak. While women-led companies now represent a smaller share of total VC deals, they continue to capture a growing portion of total capital raised, signaling stronger deal quality and investor confidence. Women co-led companies closed Q4 2025 with $24.4 billion across 716 deals (vs. $17.8 billion across 812 deals in Q4 2024)

In Q4 2025, female-only founded companies captured 6.0% of total deal count, while female-and-male co-led teams accounted for 18.0%

In terms of capital, female-only teams received 1.2% of total VC investment, compared to 39.8% going to mixed-gender founding teams

According to PitchBook data, the 16-year trend shows steady progress across states, industries, and stages, highlighting a sustained shift toward greater inclusion and visibility for women founders in the U.S. venture ecosystem

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team