What Capital Is Choosing

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: AI, Autonomy And Biotech Top The Ranks (Crunchbase, 5 minute read)

Anthropic (AI): Amazon invested $5B, with up to $20B more committed, to scale next-generation AI models and deepen its partnership around training and deploying Claude across cloud infrastructure

Reliable Robotics (Autonomous Aviation): Raised $160M to expand its autonomous aircraft systems, targeting both commercial cargo operations and defense applications as automation adoption accelerates

Ray Therapeutics (Biotech): A $125M Series B will fund clinical development of gene therapies aimed at restoring vision, building on its broader $247M in total funding to date

Omni (AI Analytics): Secured $120M at a $1.5B valuation to scale its AI-powered analytics platform, helping enterprises streamline data workflows and decision-making

Tortugas Neuroscience (Biotech): Closed a $106M Series A to advance novel treatments for neurological disorders, backed by leading life sciences investors

What The Record Venture Funding Quarter Actually Means For Your Startup’s Fundraise (Crunchbase, 4 minute read)

Q1 2026 saw a record $300B in venture funding, but 65% ($188B) went to just four companies, highlighting extreme concentration at the top. However, the broader market tells a different story: early-stage funding rose 41% YoY, and AI/ML deal count reached 6,678 in 2025 (up from ~5,600), showing continued activity at the startup level. The key shift is structural:

Horizontal SaaS is down 35%, while vertical SaaS is up 3%, as AI commoditizes general tools but increases the value of industry-specific solutions

At the same time, AI is expanding the software market from roughly $0.5T toward $6T+, as it captures more knowledge-work functions

Exit dynamics are shifting: ~2,300 M&A vs. 65 IPOs in 2025, with $200B in negative VC cash flows, pushing founders toward acquisitions

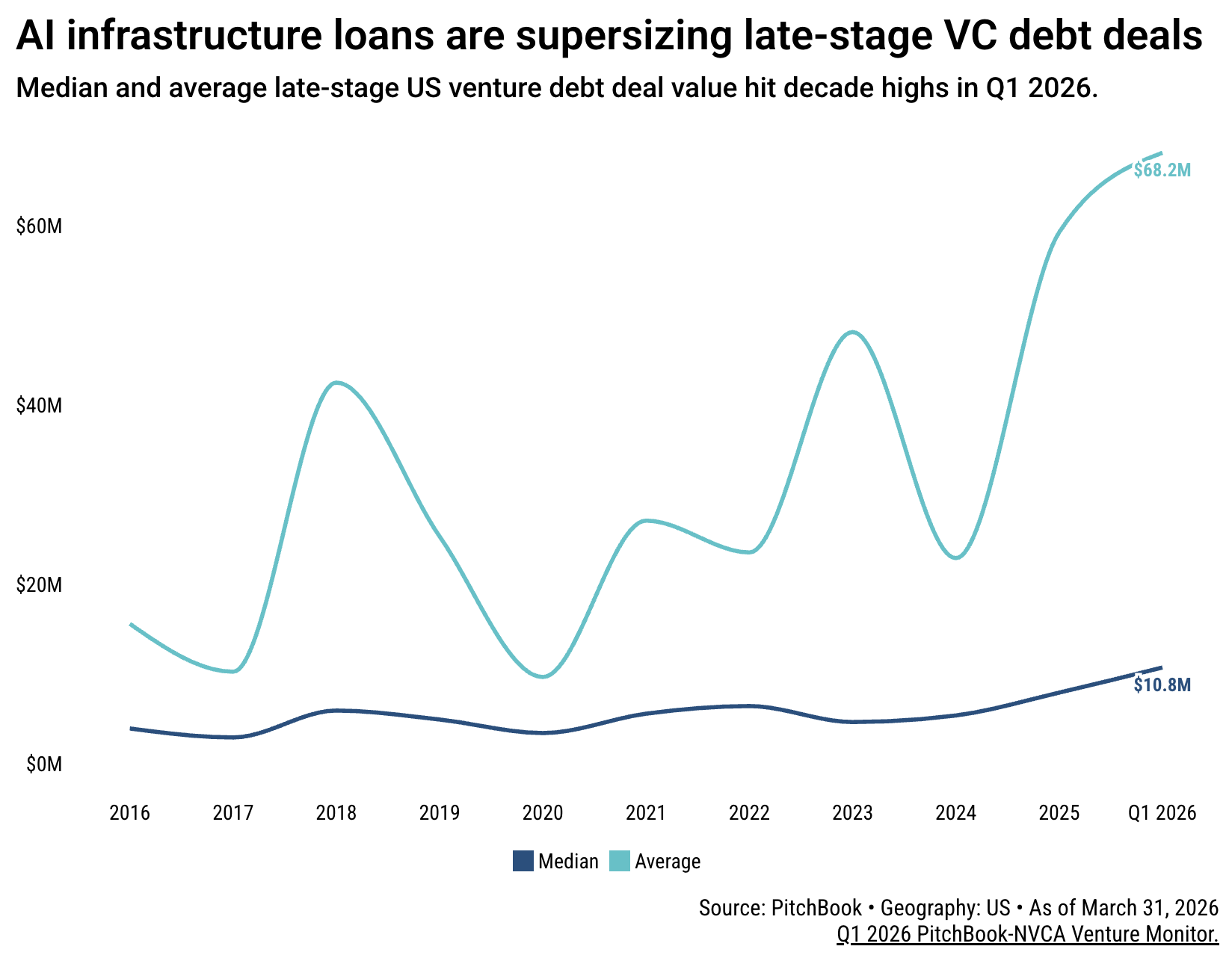

Late-stage venture debt hits decade highs as AI startups turn to lenders over equity (PitchBook, 3 minute read)

Venture debt is shifting toward late-stage startups, reaching a decade high in Q1 2026, with median deals at $10.8M and averages at $68.2M. Growth companies accounted for 67% ($13.3B) of U.S. venture debt, driven largely by AI firms financing capital-intensive infrastructure like data centers and chips

Large AI companies are taking on significant debt to avoid equity dilution, for example, SpaceX increased debt to $23B (from $14B), while OpenAI ($4B debt) and Anthropic ($2.5B debt) also combine large equity raises with borrowing

While lenders are comfortable with these high-growth, near-exit companies, risk is rising due to heavy loan concentration in a small number of AI players

ECONOMIC SNAPSHOT

Tariff refunds begin on Monday. These retailers are due big paydays (CNBC, 5 minute read)

U.S. importers are set to receive $160B+ in tariff refunds following the Supreme Court ruling, with claims opening through the CAPE portal, though companies expect the process to be slow and complex due to legal and bureaucratic hurdles. Major retailers stand to benefit significantly, Walmart ($10.2B), Target ($2.2B), Nike ($1B), with refunds potentially boosting earnings or funding buybacks and debt reduction. However, uncertainty remains

Companies may face legal risks if refunds are reclaimed after passing costs to consumers (tariffs added ~0.76pp to CPI)

The administration is also considering new tariffs (Section 301) that could partially offset the rollback

Overall, while the refunds provide a potential cash boost, execution risks and policy uncertainty remain high

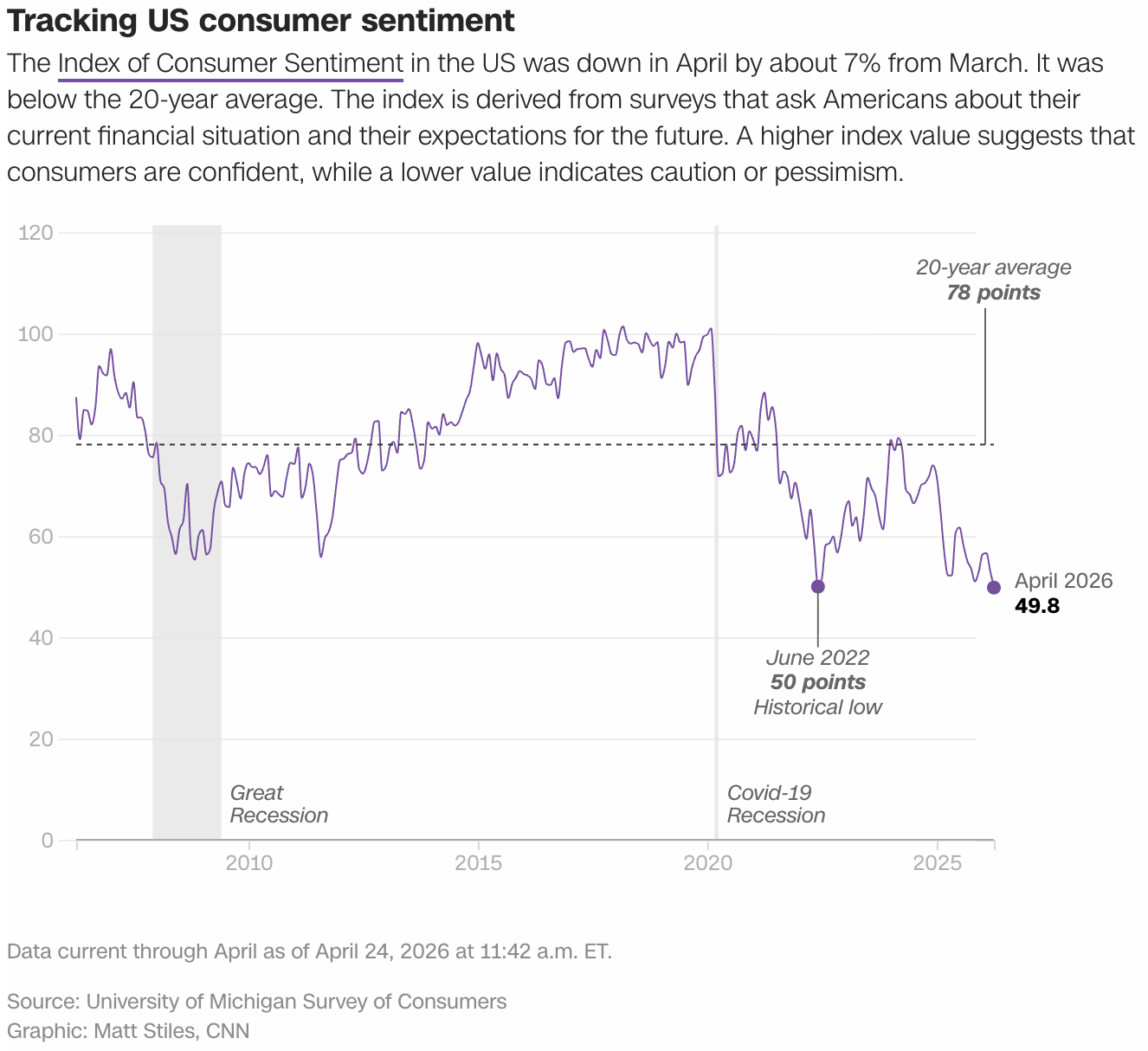

Consumer sentiment rebounds slightly after hitting lowest level on record (CNN, 2 minute read)

U.S. consumer sentiment remains extremely weak, with April’s reading at 49.8, near the lowest level since records began in 1952, reflecting ongoing concerns about inflation and economic uncertainty. Rising gas prices tied to the Iran conflict and broader cost pressures are weighing on households, with personal finances down 9% and many citing declining living standards

Inflation expectations are also worsening, with year-ahead expectations rising to 4.7% (from 3.8%), marking a sharp increase

Overall, sentiment is hovering near levels seen during the 2022 inflation peak, highlighting persistent consumer anxiety despite a brief ceasefire-driven improvement

Impact of Iran war will hurt US even after conflict ends, economists warn (Financial Times, 7 minute read)

The Iran war has triggered a renewed inflation shock in the U.S., reversing prior disinflation trends and pushing prices higher across the economy. Oil prices surged from ~$70 to $110 per barrel, while gasoline rose from $2.98 to $4.08/gallon and diesel from $3.76 to $5.59, driving U.S. inflation to 3.3% in March, the highest in two years

Inflation expectations are rising, with forecasts increasing to 3.2% (IMF) and up to 4.2% (OECD) for 2026, while consumers expect ~4.8% inflation over the next year

Beyond fuel, second-order effects are building: jet fuel has doubled, fertilizer is up 30%+, and transport costs are pushing prices higher

Even if the conflict eases, inflation is expected to stay elevated and persistent, hitting lower-income households hardest

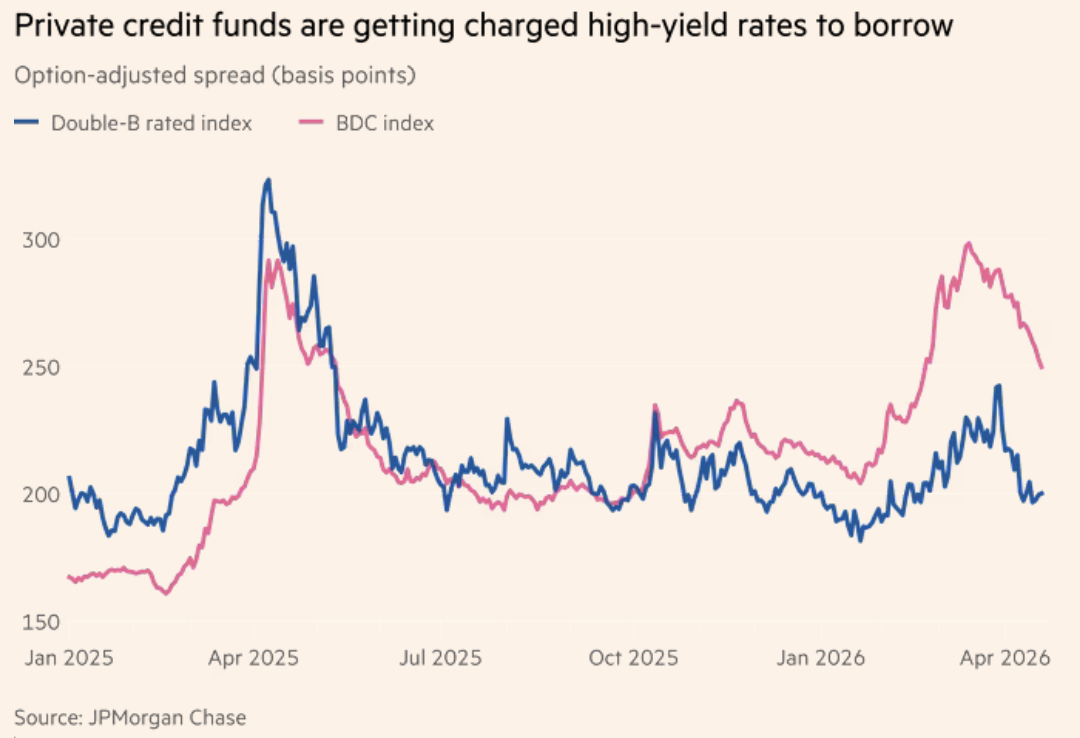

Private credit funds strained as borrowing costs edge higher (Financial Times, 5 minute read)

Private credit funds are facing rising financing pressure as borrowing costs increase and lenders tighten terms across the $2T industry. Investor-required premiums have risen +0.34pp YTD and +0.83pp since early 2025, reflecting growing concerns about credit quality, particularly in loans to tech companies. Funding activity is slowing: business development companies issued $6.8B in bonds in Q1 2026, down 22% YoY and 36% vs. 2024

At the same time, borrowing costs are climbing, e.g., Goldman Sachs Private Credit paid +2.55pp over Treasuries, significantly above comparable corporate debt spreads

Funds are shifting to cheaper financing like CLOs (e.g., Blackstone ~$450M at +1.28pp), while facing higher scrutiny and redemption pressure

Overall, the sector is dealing with higher costs, tighter liquidity, and growing risk concerns

Kevin Warsh set to lead the US economy facing a 'very wide' range of outcomes as Iran war, energy shock, and labor uncertainty loom (Yahoo Finance, 5 minute read)

If confirmed, Kevin Warsh would take over the Federal Reserve during a major energy-driven inflation shock, as the Iran war pushes up oil prices and complicates monetary policy. Higher energy costs are raising inflation while simultaneously acting as a drag on growth, creating a policy dilemma between keeping rates high to control prices or cutting them to support the economy. The impact is already visible:

Gas prices have risen above $4 per gallon, contributing to 3.3% annual inflation and a 0.9% monthly increase, the fastest since 2022

At the same time, global growth forecasts have been revised down (3.3% to 3.1%, with downside scenarios as low as 2–2.5%)

Markets expect rates to stay steady (~69% through 2026), underscoring the tradeoff between inflation and slowing growth

IPO & EXITS

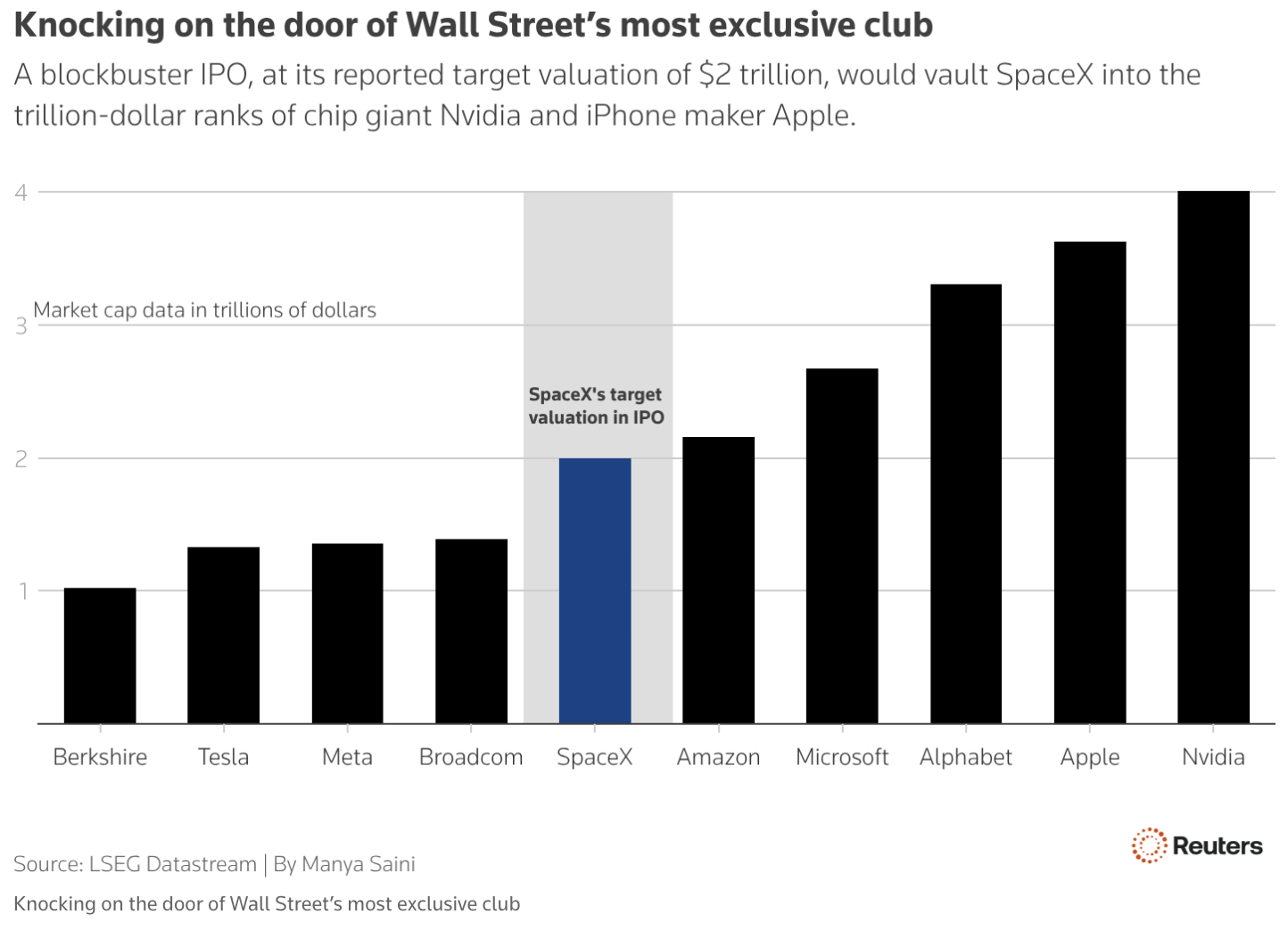

Biggest IPO wave in history promises $3 trillion in value – with no profits (Reuters, 5 minute read)

SpaceX, OpenAI, and Anthropic are poised to lead a potential $3 trillion wave of IPOs, marking one of the largest in history, but all three are currently unprofitable, an unusual combination at this scale. SpaceX alone is targeting a $1.75T valuation (with ~$18.6B revenue and ~$5B loss), while OpenAI is seeking around $1T and Anthropic was last valued at $380B. These listings reflect strong investor appetite for high-growth AI companies

This mirrors the dominance of the “Magnificent Seven,” which now make up ~33% of the S&P 500 and have delivered significantly higher earnings growth than the rest of the index

However, without sustained profitability, these companies risk delayed S&P 500 inclusion, limiting access to $20T+ in passive capital

These IPOs test whether markets will support high valuations without profits, potentially increasing concentration

The IPO Pipeline Finally Gets Interesting (Crunchbase, 4 minute read)

IPO activity among venture-backed startups is picking up, with several companies moving from speculation to public S-1 filings, signaling real intent to go public. Leading the wave is Cerebras Systems, targeting a ~$2B raise at a $35B+ valuation, potentially the largest U.S. semiconductor IPO. Other notable debuts include X-energy raising ~$1B (shares up 27% on day one), Fervo Energy targeting ~$250M, and multiple biotech firms such as Kailera Therapeutics ($718M)

The pipeline is expanding across sectors — biotech, clean energy, defense, and space, with SpaceX reportedly targeting a ~$1.75T valuation

However, enterprise software remains notably absent, reflecting investor concerns about AI disruption

Overall, while the IPO market is still selective, activity is broadening beyond its recent slowdown

Secondaries’ next layer raises old questions (PitchBook, 5 minute read)

The private equity secondaries market has grown so large that it is now driving demand for “tertiary funds”, vehicles that buy stakes in secondary funds, adding another layer to the liquidity chain. While still niche, the segment is scaling quickly, with firms like Netley Capital expanding to $825M (up from $315M)

These funds provide liquidity to LPs, but add more complexity, less transparency, and extra fees by layering additional intermediaries between investors and the same underlying assets

In some cases, tertiary funds invest in transactions ranging from $5M to $1B, further highlighting the scale and variability of the market

The rise of tertiary funds reflects persistent liquidity constraints in private markets

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team