Bigger Bets, Fewer Winners

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: A Varied Week For Big Deals, Led By AI And Defense (Crunchbase, 5 minute read)

OpenAI (AI): Raised an additional $10B, bringing its total round to $120B+, one of the largest private fundraises ever. Backers include a16z, D.E. Shaw, MGX, TPG, and T. Rowe Price, reinforcing its dominance in foundational AI and positioning it closer to a potential IPO

Shield AI (Defense Tech): Raised $2B at a $12.7B valuation, including $1.5B Series G + $500M preferred equity from Advent, JPMorgan, and Blackstone. Capital will partly fund the acquisition of Aechelon Technology, expanding its capabilities in military training simulations and autonomous defense systems

Cambridge Mobile Telematics (Mobility/AI): Secured $350M, bringing total funding to $850M+. The company focuses on telematics and AI-driven safety solutions for insurers and mobility platforms, reflecting growing investment in data-driven risk and insurance tech

Harvey (Legal Tech): Raised $200M at an $11B valuation, with total funding reaching ~$1.2B. Backed by GIC and Sequoia, Harvey is rapidly scaling AI tools for law firms and in-house teams, signaling strong demand for vertical AI applications in professional services

eMed (Healthcare): Raised $200M at a $2B+ valuation, led by Aon, to expand its GLP-1 and employer-focused healthcare programs. The company targets corporate wellness and chronic care management, tapping into rising demand for weight-loss and preventative health solutions

AI startups are eating the venture industry and the returns, so far, are good (TechCrunch, 4 minute read)

AI startups are dominating venture capital, accounting for 41% of the $128B raised on Carta in 2025, with funding highly concentrated as 10% of startups captured ~50% of total capital. This surge is driven by massive rounds from leading players like OpenAI ($110B), xAI ($20B), and Anthropic ($30B at a $380B valuation), which together made up a significant portion of the $189B in global VC funding last month and are signaling potential IPOs

The market has become K-shaped, with fewer startups raising capital but at much larger sizes due to the high costs of building and running AI models

Meanwhile, newer funds (2023–2024 vintages) are showing strong early IRRs, partly fueled by AI exposure and valuation markups

However, these returns remain largely unrealized and depend on future exits, raising questions about whether this reflects sustainable performance or early-stage hype

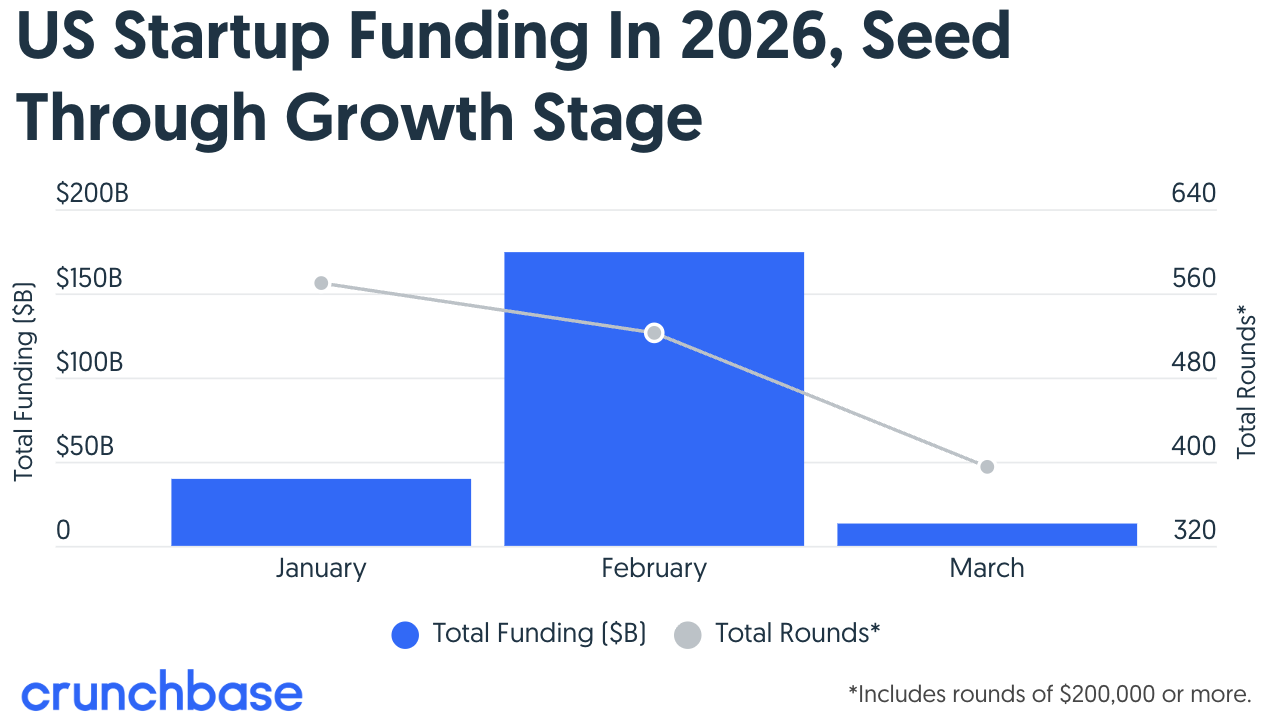

US Startup Funding Slows Sharply In March (Crunchbase, 3 minute read)

U.S. startup funding fell sharply in March to around $13B, a steep drop from February’s record levels, driven primarily by the absence of mega-rounds such as OpenAI’s $110B, Anthropic’s $30B, and Waymo’s $16B. The slowdown is concentrated at the late stage, while seed and early-stage funding remained relatively stable compared to prior months. The decline also coincides with geopolitical tensions following the Feb. 28 Iran War and broader market volatility, which have weighed on investor sentiment and stock markets

However, the slowdown appears largely U.S.-specific, as European startup funding reached its highest level of the year in March, boosted by major AI deals

Overall, February’s outsized funding, heavily skewed by a single $110B round, sets a benchmark unlikely to be repeated in the near term

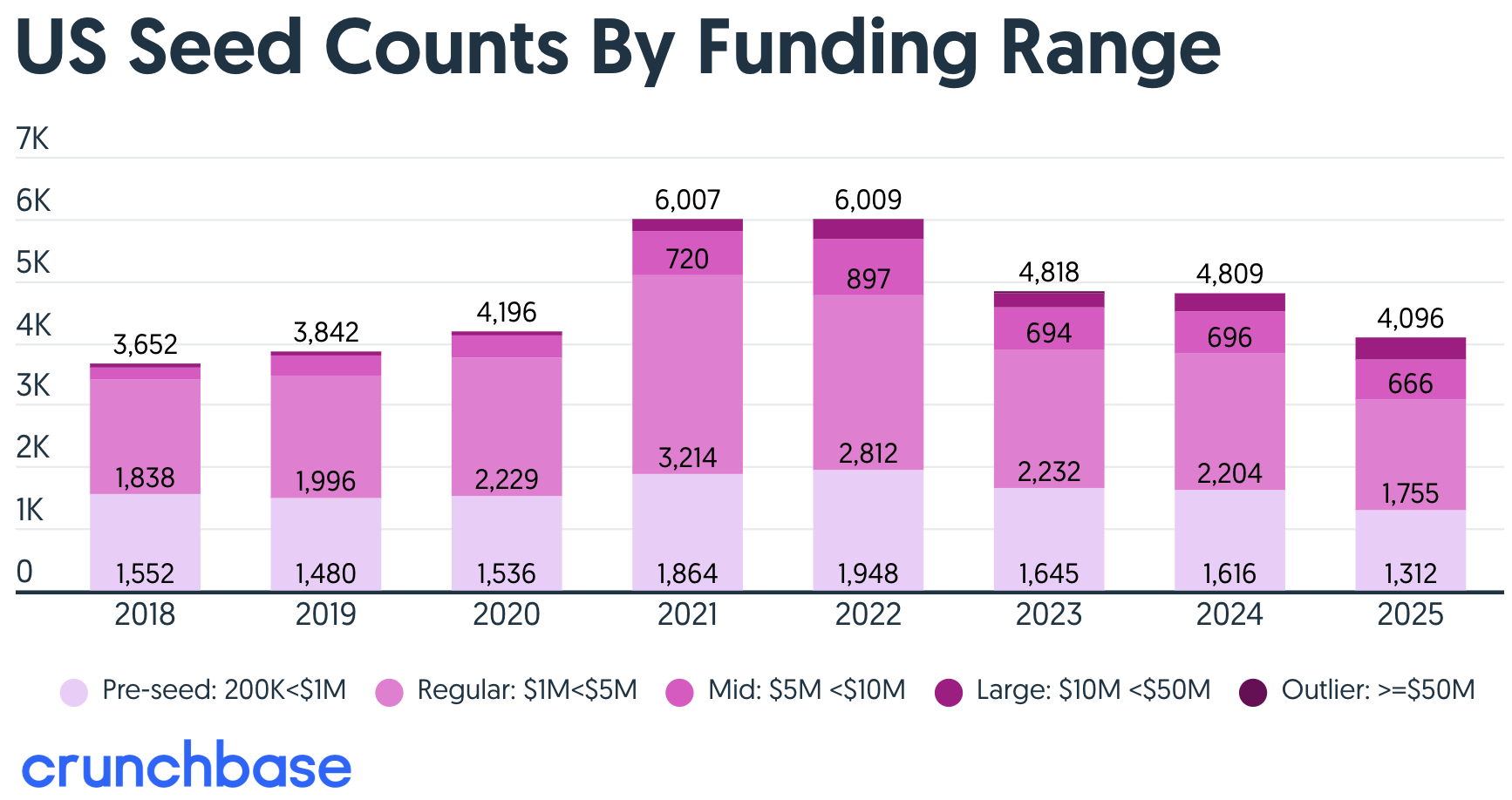

Seed Funding Hasn’t Stalled, But It’s Skewing Larger And Is More Competitive Than Ever, Crunchbase Data Shows (Crunchbase, 4 minute read)

U.S. seed funding reached $19.4B in 2025, but the market has become increasingly bifurcated, with capital concentrating in larger rounds. Smaller seed deals ($200K–$5M) saw ~20% declines YoY, while mid-sized rounds ($5M–$10M) remained flat and larger rounds ($10M+) grew significantly. The share of small deals dropped from 93% (2018) to 75% (2025), while large seed rounds ($10M+) rose from 2% to 9% (~360 deals)

Larger rounds now dominate funding, accounting for 51% of total seed capital (vs. ~33% in 2024), with outlier rounds ($50M+) increasing 300%+

Overall, AI is reshaping seed investing by driving larger, earlier bets on top teams, while smaller funds invest earlier and reserve more capital, reinforcing a winner-takes-most market

ECONOMIC SNAPSHOT

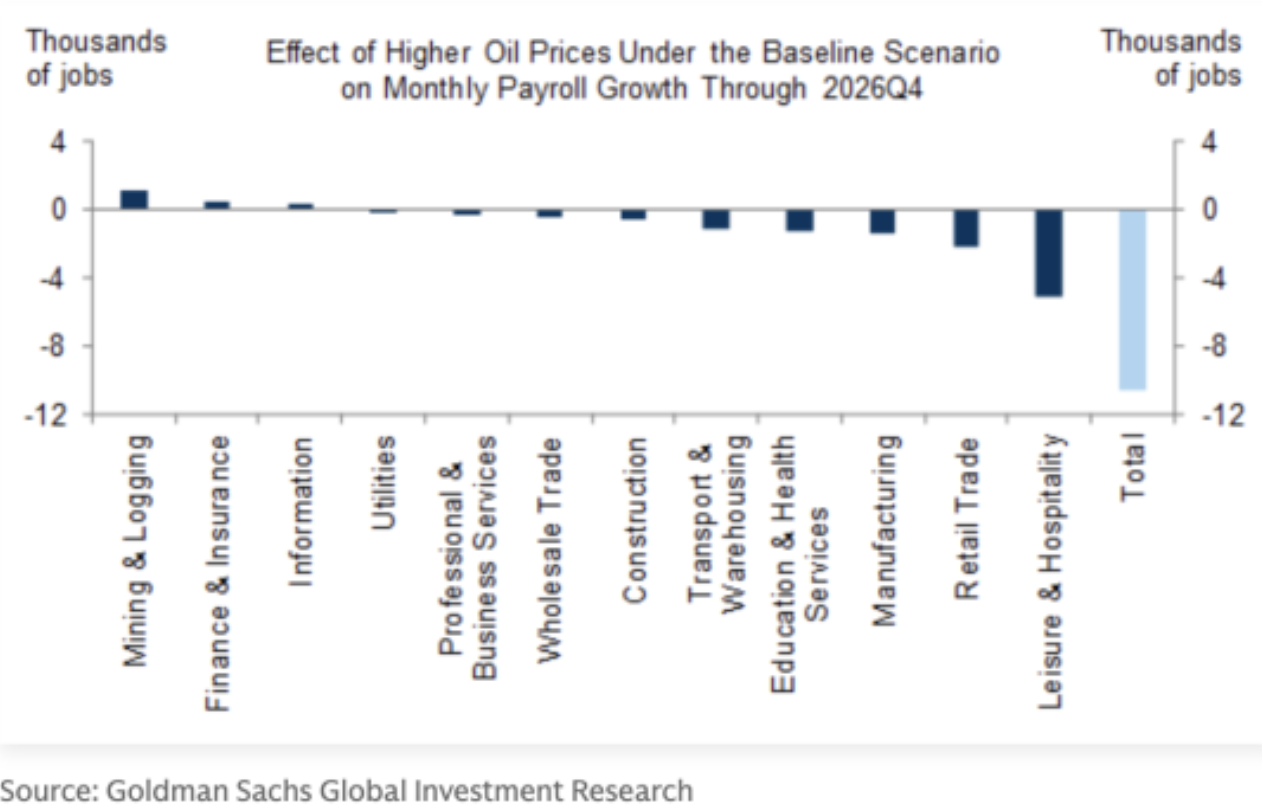

Trump’s war in Iran is costing the U.S. economy 10,000 jobs a month, Goldman Sachs says (Fortune, 4 minute read)

The U.S.-Iran conflict is expected to weigh on the U.S. labor market, with Goldman Sachs estimating a loss of ~10,000 jobs per month through year-end due to rising oil prices. Energy shocks could push Brent crude to $115–$140+ per barrel, driving higher consumer costs and reducing discretionary spending, particularly impacting leisure and hospitality (~5,000 jobs lost/month) and retail (~2,000/month)

The broader effect could lift U.S. unemployment to ~4.6% by Q3 2026

Younger workers, especially Gen Z, are expected to be disproportionately affected due to higher exposure to both fuel costs and service-sector jobs

While the U.S. economy is more resilient to oil shocks, limited job growth in the energy sector means the impact on employment and growth will still be significant

Dow closes in correction, S&P logs longest weekly losing streak in four years and oil settles at Iran-war highs (CNN, 3 minute read)

As of March 27, U.S. markets fell sharply amid rising oil prices and uncertainty around the Iran war, with the Dow dropping 793 points (-1.73%) and entering correction territory (-10% from peak), while the S&P 500 (-1.67%) and Nasdaq (-2.15%) also hit multi-month lows. The Nasdaq is now down ~12.5% from its peak, and the S&P 500 is ~8.7% below its high, reflecting pressure on tech and growth stocks

The selloff was driven by surging energy prices, with Brent at ~$112.6 and WTI near $100

It was also fueled by rising bond yields (10-year ~4.43%, briefly 4.48%; 30-year near 5%), signaling higher inflation and interest rate expectations

Markets have now declined for five consecutive weeks, with sentiment in “extreme fear” territory, highlighting growing macro and geopolitical concerns

Private Credit Is Reeling, But New Rule May Allow It Into 401(k)s (The Wall Street Journal, 5 minute read)

The Trump administration has proposed a rule to open the $14.2T U.S. 401(k) market —retirement savings accounts where employees invest in funds like stocks and bonds— to private equity, private credit, and other alternative assets, aiming to reduce litigation risks that have historically limited their adoption. The regulation introduces a safe harbor framework with six evaluation criteria (including fees, liquidity, and performance) and excludes certain structures like continuation funds, while a 60-day public comment period precedes finalization

While the move is a win for private markets seeking retail access amid fewer public companies, adoption is expected to be gradual due to concerns around higher fees, lawsuits, and recent pullbacks in private credit

Broader uptake will likely depend on participation from major target-date fund providers

Private credit’s moment for a healthy reset (Financial Times, 4 minute read)

Private credit is facing a sharp downturn, with sell-offs in business development companies and withdrawal limits from major funds like Apollo and BlackRock, raising concerns about the $2T global market. Fears are driven by exposure to vulnerable sectors, over 25% tied to industries at risk from AI disruption, along with rising interest rates and weakening credit quality, with defaults potentially reaching ~8% (vs. ~2% historical average)

Market stress is clear, with BDCs trading at ~82% of net asset value, while institutional exposure remains high, including ~1/3 of U.S. life insurer assets in private credit

Despite this, systemic risk appears limited given the market’s smaller scale relative to $50T+ global bank lending and only ~5% exposure in U.S. bank loan portfolios

Overall, this points to a correction rather than a full-blown crisis

IPO & EXITS

Nasdaq Speeds Up Index Entry for SpaceX, Large IPOs With New Rule (Bloomberg, 3 minute read)

Nasdaq will implement a rule change (effective May 1) allowing large IPOs to join the Nasdaq-100 in ~15 days (vs. 3+ months previously), while removing the 10% float requirement. Eligibility applies to companies whose market caps rank among the index’s largest members, accelerating entry for mega-cap listings. The move reflects pressure to adapt to larger, later-stage IPOs, such as a potential $1.75T SpaceX listing, and aligns with similar considerations by S&P and FTSE Russell

With over $30T in assets benchmarked to major indexes, faster inclusion could significantly accelerate passive capital flows into newly public companies

It could also reshape how wealth transitions from private to public markets

Exclusive: Musk rewrites IPO playbook with large slice of SpaceX stock for retail investors, source says (Reuters, 4 minute read)

SpaceX is planning an unconventional IPO that could allocate up to 30% of shares to retail investors, far above the typical 5–10%, tapping into strong demand from individual investors and Musk’s loyal following. The company is expected to debut at a valuation of up to $1.75T, potentially making it one of the largest companies in the Nasdaq-100 and rivaling the scale of the $29B Saudi Aramco IPO

In parallel, SpaceX is restructuring the traditional IPO process by assigning banks specific roles by geography and investor type (e.g., Morgan Stanley via E*Trade for retail, Bank of America for U.S. high-net-worth), rather than broad competition

The strategy aims to build a more stable shareholder base, reduce post-IPO volatility, and reshape how capital is distributed in mega-listings

WHAT A TIME TO BE ALIVE

The best AI investment might be in energy tech (TechCrunch, 5 minute read)

AI investment has exceeded $500B over the past five years, but a major bottleneck is emerging in energy and power infrastructure, with up to 50% of data center projects facing delays due to limited electricity access. Of the roughly 190 GW of planned data center capacity, only 5 GW is currently under construction, while just 6 GW came online last year and 36% of projects experienced delays in 2025, highlighting a widening supply-demand gap. With AI expected to drive a 175% increase in data center power demand by 2030, large tech companies like Google and Meta are investing heavily in solar, wind, nuclear, and battery storage, while also exploring on-site and hybrid power solutions, which already represent 44% of capacity among projects with identified power sources

This constraint is creating a significant investment opportunity in energy infrastructure, including grid-scale batteries (projected ~65 GW U.S. capacity by year-end), power management software, and next-generation transformers

It is also driving investment into startups focused on power conversion and grid optimization

Overall, energy is emerging as a critical “picks and shovels” layer of the AI boom, and potentially a more resilient investment thesis than AI itself

Equal Pay Day 2026: The ‘Bonus Gap’ And More Wage Gap Contributors (Forbes, 4 minute read)

Equal Pay Day 2026 falls on March 26, meaning women must work nearly 3 extra months to match men’s prior-year earnings, reflecting an average gap of about $13,570 annually and roughly 81 cents on the dollar. Over a 40-year career, this compounds to losses of about $542,800 for women and $1M+ for women of color, with the gap widening for mothers and those in lower-paying sectors

The disparity is driven by structural factors such as occupational segregation, caregiving burdens, and lack of paid leave

It also persists within similar roles, where ~1/3 of the gap is unexplained and attributed to discrimination

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team