The Economics of Conflict

Welcome to AI8’s weekly newsletter, your ultimate source for curated insights and updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: AI, Robotics And E-Commerce Top The Ranks (Crunchbase, 5 minute read)

Quince ($500M, e-commerce): The San Francisco–based affordable luxury retailer raised $500M in Series E funding led by Iconiq Capital, valuing the 8-year-old company at $10.1B post-money

Nexthop AI ($500M, AI infrastructure): Lightspeed Venture Partners led a $500M Series B for the Santa Clara startup building open-source networking switches for AI and cloud data centers, with Andreessen Horowitz among the investors

Mind Robotics ($500M, robotics): Co-led by Accel and Andreessen Horowitz, the $500M Series A will support the Rivian spin-out’s efforts to develop AI-powered industrial robotics systems for large-scale manufacturing automation

Rhoda AI ($450M, robotics): The Palo Alto startup emerged from stealth with $450M in Series A funding reportedly led by Premji Invest, using hundreds of millions of videos to train robots for complex real-world environments

Replit ($400M, AI software): The Foster City–based AI software creation platform secured $400M in Series D funding led by Georgian, boosting its valuation to $9B, triple its $3B valuation from six months earlier

VC mega-funds are back with General Catalyst, Spark rumored to be raising billions (TechCrunch, 3 minute read)

Venture capital firms are raising massive new funds in 2026, highlighting strong investor demand for startup exposure, particularly in AI. General Catalyst is reportedly seeking to raise $10B, following Thrive Capital’s recent $10B fund, double its previous one. Earlier in the year, Andreessen Horowitz announced $15B in new funds, one of the largest raises in the sector

These fundraising efforts come even as venture firms were already sitting on record levels of dry powder at the end of 2025

The influx of capital suggests venture investors will continue deploying large rounds, especially for AI startups, where billion-dollar valuations and oversized early-stage funding rounds are increasingly becoming the norm

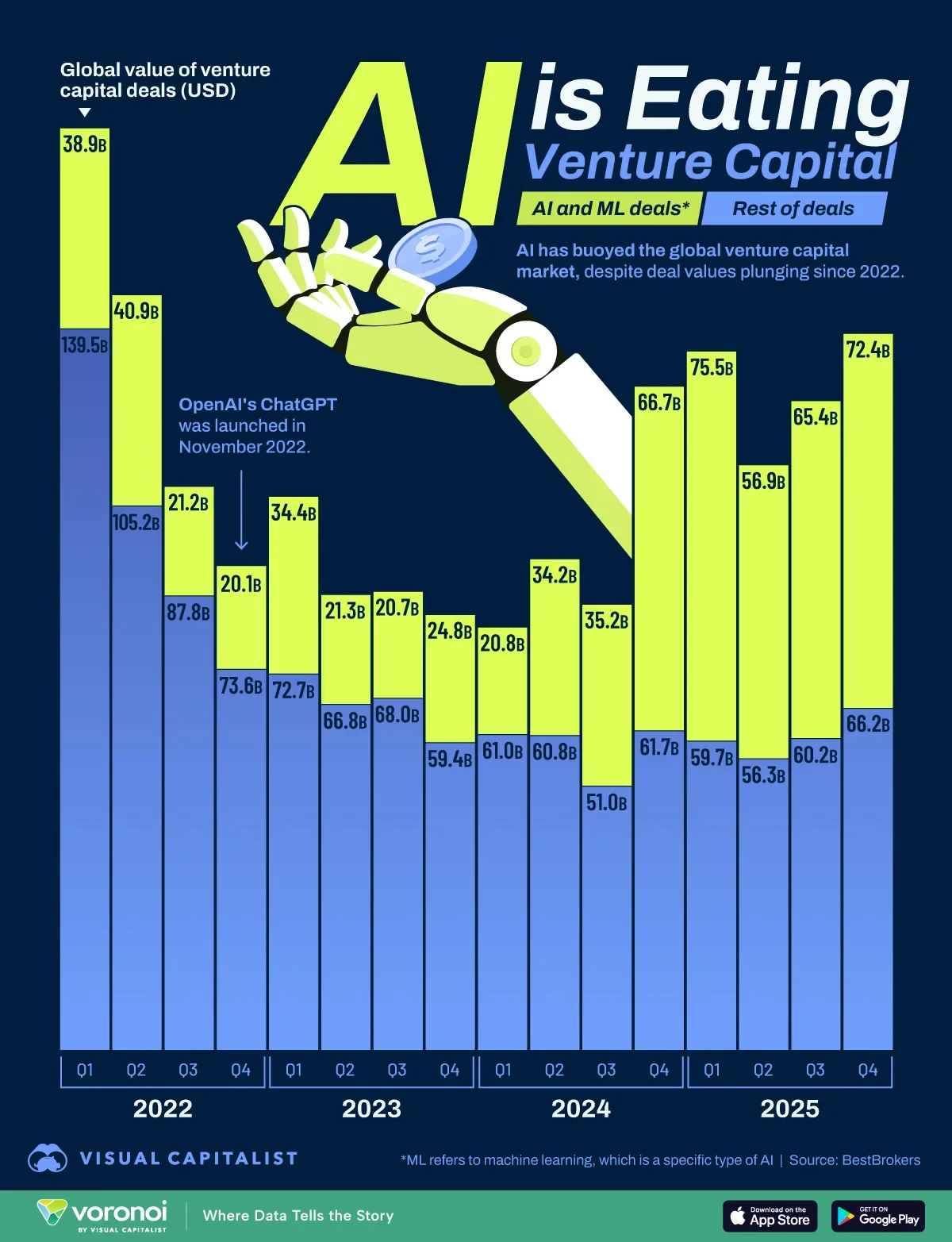

Where Venture Capital Money Is Going: AI vs. Everything Else (Visual Capitalist, 4 minute read)

AI has become the dominant force in venture capital. Funding for AI and machine learning has surged over the past two years, helping sustain overall VC activity even as investment in other sectors cooled. By Q4 2025, AI accounted for 52% of global venture deal value, marking the first time the sector represented more than half of total funding. Venture deals totaled $138.6B globally that quarter, with $72.4B going to AI companies compared with $66.2B across all other sectors combined

The shift began after OpenAI launched ChatGPT in November 2022, accelerating investor interest in generative AI despite a broader venture slowdown

The surge came in 2024 as massive rounds flowed into AI infrastructure and model developers, pushing quarterly investment to $66.7B in Q4, exceeding the rest of the market

While enthusiasm remains high the concentration of venture capital around AI has also raised concerns about a potential bubble and opaque private deal structures

ECONOMIC SNAPSHOT

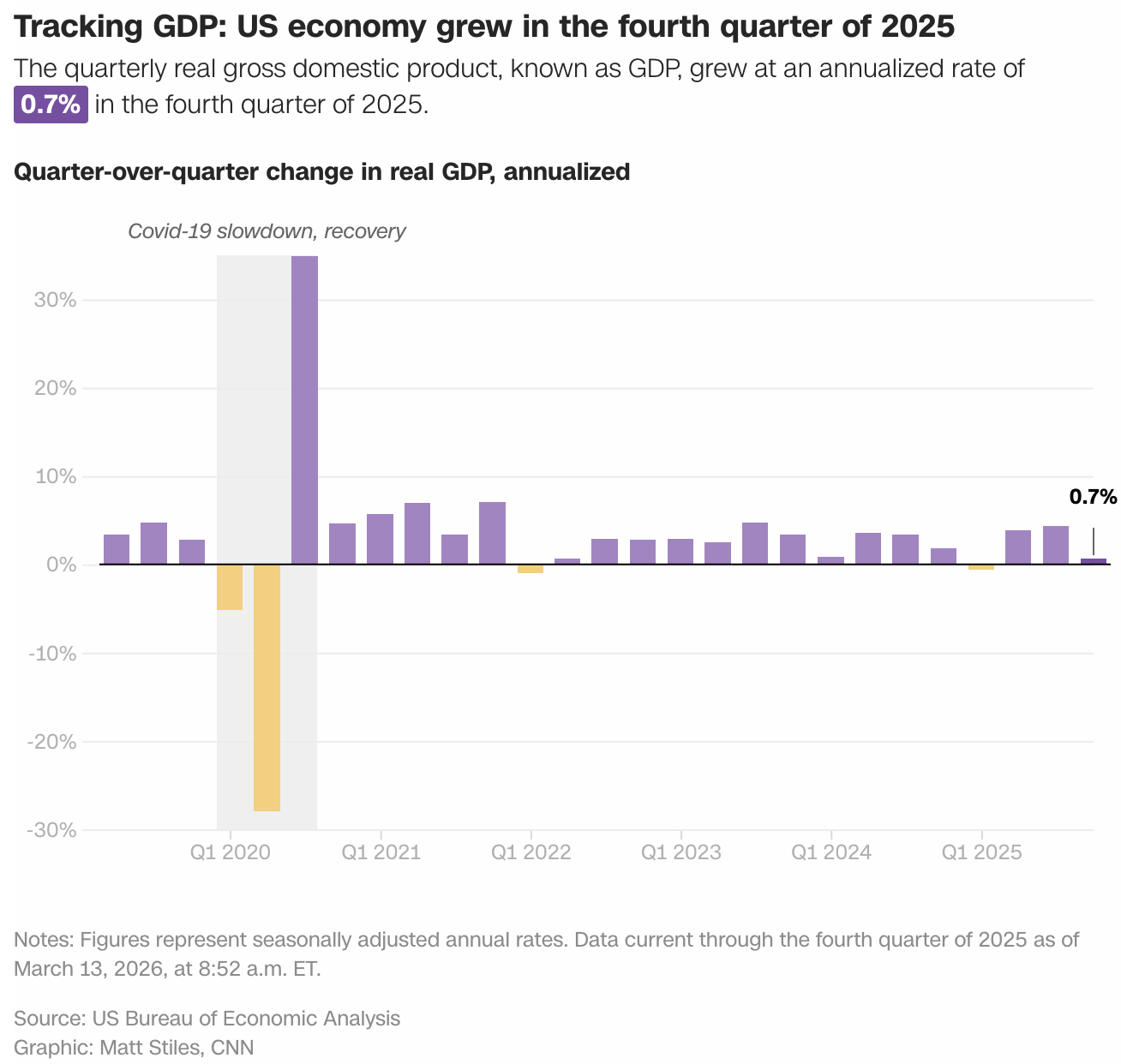

The US economy grew just 0.7% last quarter, ahead of a potentially destabilizing war with Iran (CNN, 4 minute read)

New data shows the U.S. economy was already weakening before the Iran war, raising concerns that the conflict could worsen inflation and slow growth. GDP grew only 0.7% in Q4 2025, sharply down from 4.4% in Q3, partly due to the government shutdown and weaker exports and consumer spending. At the same time, the labor market remains fragile, with 92,000 jobs lost in February and unemployment rising to 4.4%, while layoffs edged higher even as job openings increased. Inflation remains a key concern

The Fed’s preferred PCE index stands at 2.8% annually, and economists warn that rising energy prices from the Iran conflict could push inflation higher

This mix of weak growth, labor market uncertainty, and rising inflation is putting pressure on the Federal Reserve

US Economy Lost Some Momentum, Inflation Held Firm Ahead of War (Bloomberg, 4 minute read)

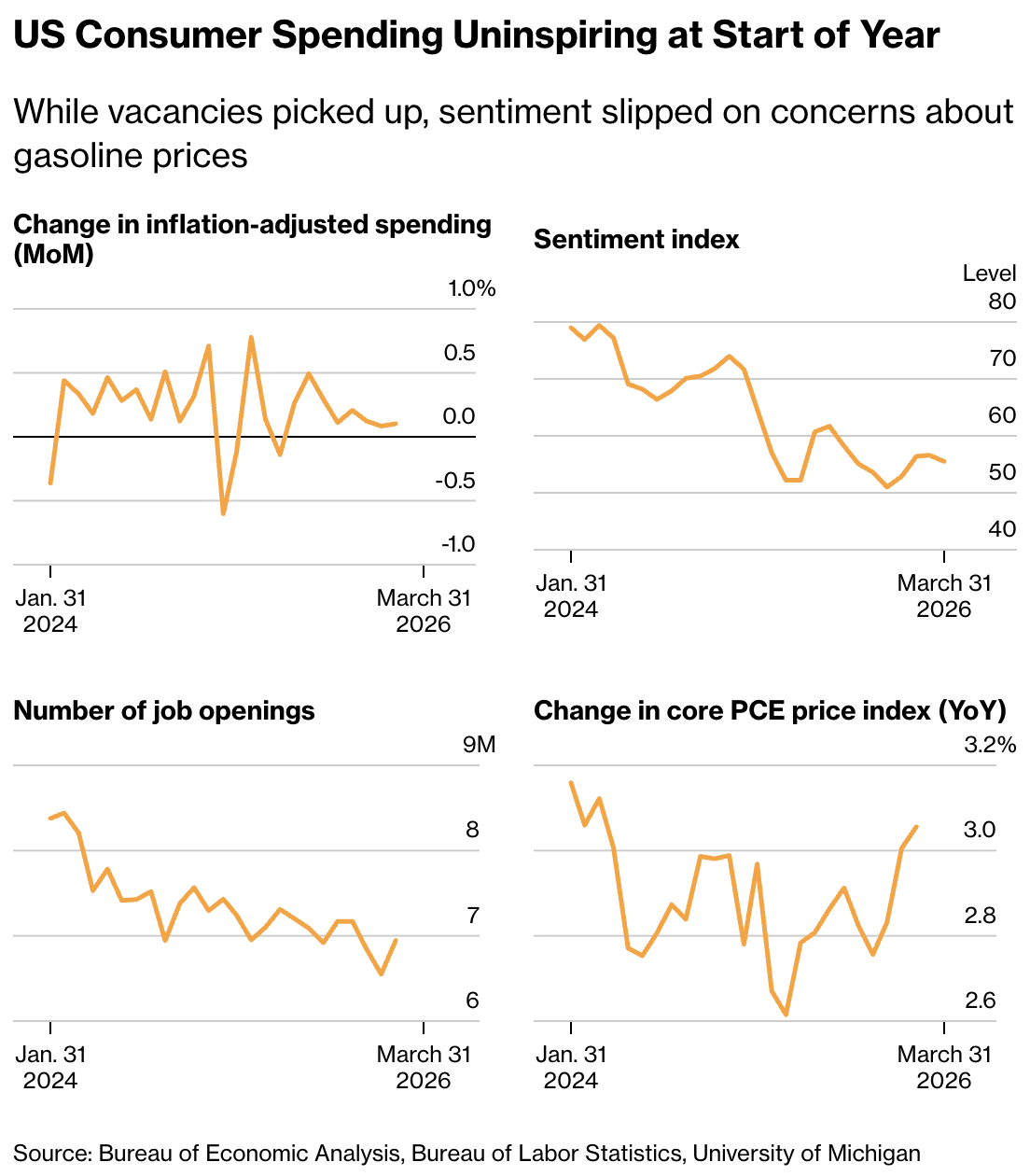

U.S. consumer spending rose just 0.1% in January (inflation-adjusted), indicating weak momentum in household demand at the start of the year. Spending on goods declined after the holiday season, while households continued spending on essential services such as healthcare, housing, and insurance, with higher-income consumers carrying much of the overall demand

Inflation pressures remain elevated, with the core PCE index rising 0.4% month-over-month and 3.1% year-over-year, the highest in nearly two years

Although incomes increased and the savings rate jumped, supported by cost-of-living adjustments and tax refunds, economists warn that higher energy prices, inflation, and labor market uncertainty could weaken consumer spending

These pressures could reduce household demand and weigh on overall economic growth

IPO & EXITS

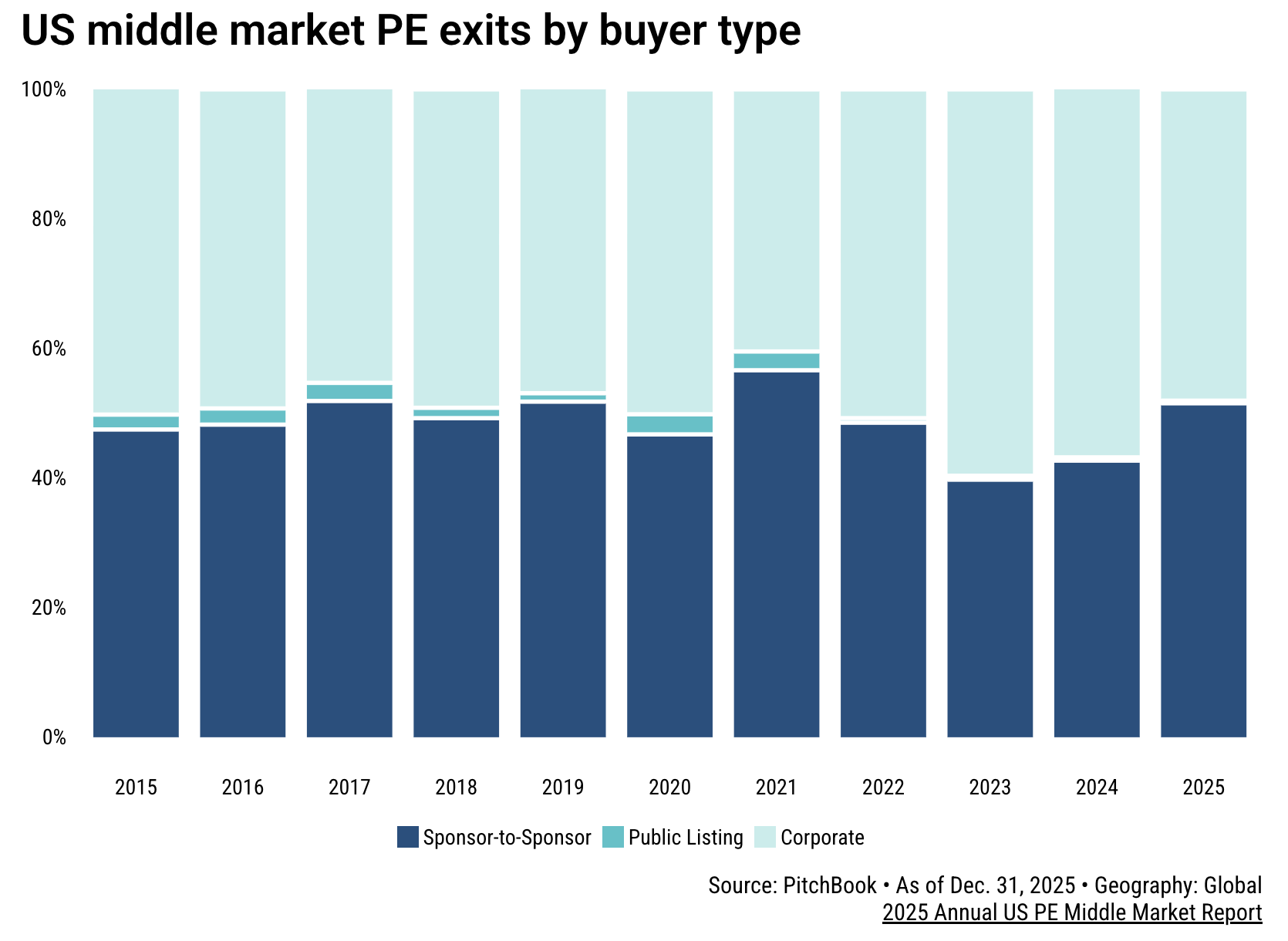

ACorporate buyers cooled on the US mid-market last year (PitchBook, 4 minute read)

Corporate buyers pulled back from U.S. middle-market private equity exits in 2025, accounting for the lowest share of exit value since 2019, according to PitchBook. Strategic buyers completed 370 exits totaling $42.2B, down 28.8% in deal count and 33.9% in value year over year. This decline came even as the overall middle-market exit environment improved, with 1,022 exits worth $140.4B in 2025. The slowdown was partly driven by valuation gaps between buyers and sellers and macro uncertainty, including inflation, tariffs, and geopolitical shocks

Corporates instead focused on larger acquisitions, with deals $1B+ accounting for 57% of the $4.93T global M&A market

Looking ahead, analysts expect corporate appetite for middle-market deals to recover in 2026, supported by stronger CEO interest in M&A and private equity managers anticipating more strategic exits

Should Hot IPOs Get Special Treatment? (The Wall Street Journal, 4 minute read)

Nasdaq is considering a rule change that could allow large IPOs, such as SpaceX, OpenAI, and Anthropic, to enter major indexes much sooner, but the proposal could also inflate their weight in those indexes beyond the shares actually available for trading. Under the proposal, if a company floats less than 10% of its shares, its index weight could be calculated at five times the value of its freely tradable stock. For example, a $1 trillion company listing only 5% of shares ($50B float) could be treated as $250B in index weight, potentially pushing it into the top tier of the Nasdaq 100

Critics warn the rule could create artificial demand from index funds, increasing volatility and distorting prices due to limited share liquidity

Supporters argue the change would allow major IPOs to join indexes faster, reflecting their economic importance

However, asset managers caution that overweighting newly public companies could increase speculation and risk for investors

Why CFOs should pay attention to Elon Musk’s SpaceX IPO—and its rumored $1.5 trillion market cap (Fortune, 4 minute read)

Elon Musk is reportedly preparing a SpaceX IPO this summer that could raise about $50B at a $1.5T valuation, potentially making it one of the largest IPOs ever and second only to Saudi Aramco in market capitalization at listing. The company has indicated about $15B in revenue and roughly $8B in EBITDA, but reports suggest it recorded a $2.4B loss in the first nine months of 2025, implying limited or no GAAP profitability at the time of the offering

At that valuation, analysts estimate SpaceX would eventually need profits exceeding those of companies like Berkshire Hathaway to justify the price

The IPO would largely be a bet on long-term growth in space infrastructure and AI rather than current earnings

It could also reset expectations for valuations and capital raising across sectors such as space, AI, and advanced technology infrastructure

SpaceX, OpenAI Potential Blockbuster IPOs Lure Investors Into Murky Deals (Bloomberg, 4 minute read)

Demand for shares in private tech giants like SpaceX, OpenAI, and Anthropic has surged, pushing wealthy investors toward special purpose vehicles (SPVs) that offer indirect access to private shares before potential IPOs. SPV investment has grown rapidly, increasing 11× since 2021 and attracting over $1.5B last year, as investors hope to profit from possible valuation jumps when these companies go public. However, the market has become increasingly opaque and risky

Some SPVs charge high fees (around 1.2–1.5% management and 13–15% carry), while others create layered structures that dilute returns

In some cases, investors may not actually own the shares they believe they purchased, and authorities have already uncovered fraud cases involving millions of dollars

As blockbuster IPOs approach, the surge in demand for private shares has created a “wild west” environment where due diligence and transparency vary widely

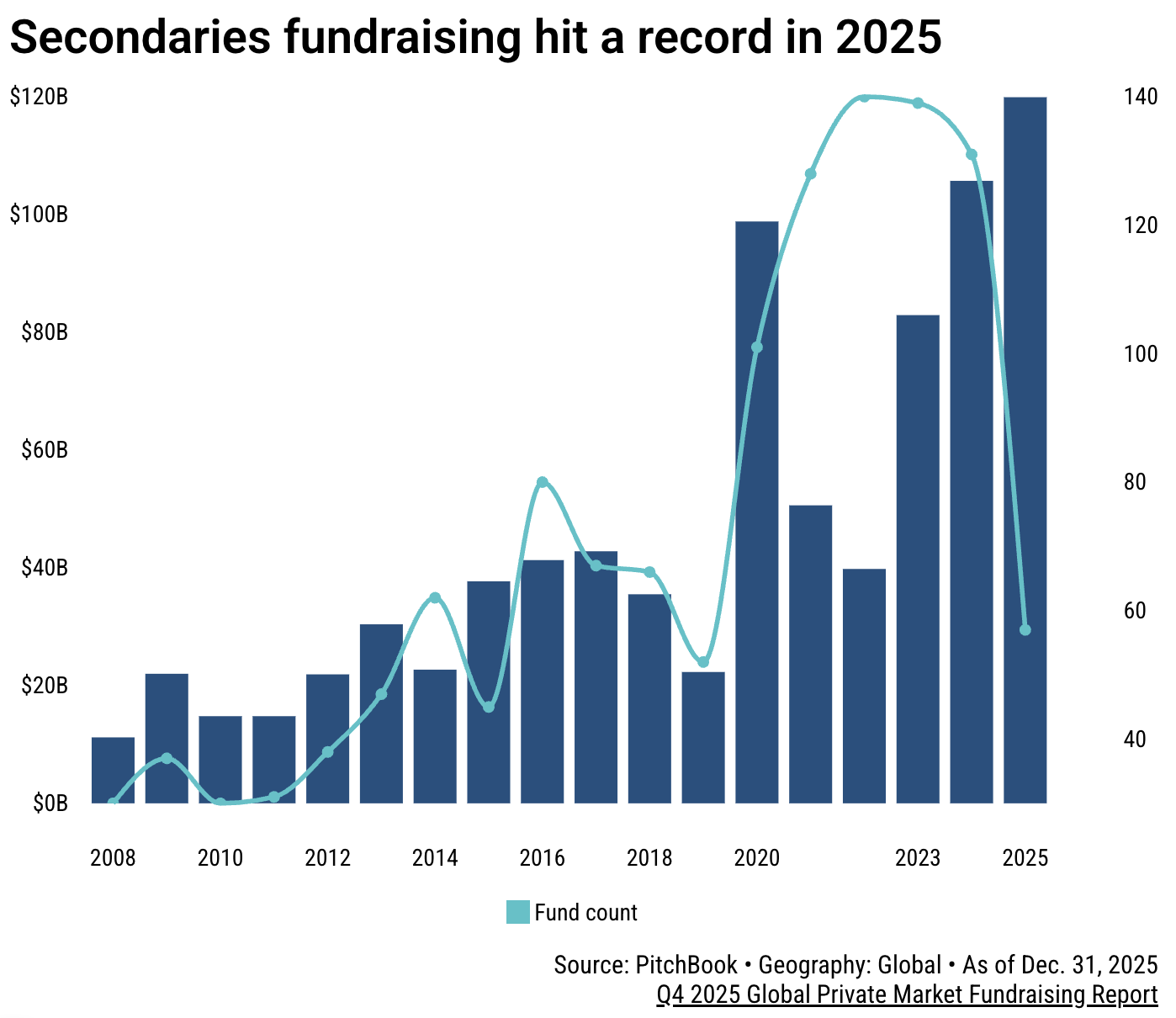

Charlesbank buys stake in Overbay to ride the secondaries boom (PitchBook, 4 minute read)

Charlesbank Capital Partners acquired a minority stake in Overbay Capital Partners, a Toronto-based secondaries investor with about $3B in assets under management, as asset managers increasingly move into the rapidly growing secondaries market. The deal comes amid a surge in secondaries activity as investors seek liquidity in private markets with limited exits

Global secondary transaction volume reached a record $240B in 2025 (up 48% year-over-year), while fundraising hit $120B, also a record

Growing interest in the sector has sparked consolidation and investment in secondaries firms

Major deals include EQT’s acquisition of Coller Capital, alongside rising M&A activity across the industry

WHAT A TIME TO BE ALIVE

Women-led startups get under 2% of global VC funding, says report (Fortune India, 3 minute read)

Women-led startups continue to receive a disproportionately small share of venture capital globally, securing less than 2% of total funding, according to the Arise Ventures Diversity Report 2026. In the U.S., women-only founding teams receive roughly 1% of venture funding, while mixed-gender teams capture about 25%, highlighting a persistent global funding gap. Despite this disparity, diverse founding teams often outperform financially

Women-led startups generate about 10% more revenue, deliver up to 20% higher net IRR, and achieve around 35% higher ROI, while expanding into 70% more new markets than non-diverse teams

The report also highlights growing opportunities in sectors such as AI, healthcare, climate tech, and consumer technology, including femtech (projected to exceed $100B by the end of the decade) and digital health (expected to surpass $1.5T by 2032)

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team